- Login to the Income Tax Portal

- login using id and password

- Now click on My Account - Reporting Portal - Confirm

- Now you will redirect to Income Tax reporting portal page

- Here click Ok then choose Manage Principal Officer then click on Continue

- Here select the Form Type and ITDREIN

- Now Choose existing DDO name then click on Deactivate

- Now close the Tab

- Now go the the Income Tax portal and do the Point 3, 4, 5 and 6 again

- Here you have to enter Principal Officer details

- After entering Principal Officer details go the Income Tax Reporting Portal

- Here click on Forgot Password

- Now enter new DDO PAN number and generate a new password using OTP

- After sucessful generating password login to the Income Tax Reporting Portal

- Now you only login using Principal officer, you have to Add Designated Director

- First go to Profile - Registered user

- Here deactivate the old DDO from Designated Director and Add new Designated Director

- Now login using Designated Director and upload the digital signatur

HOW TO ADD NEW DDO DETAILS IN SFT FILING

How to upload TDS statements on Income Tax e-Filing Portal

To Upload TDS, the steps are as below:

- Create Signature file for registering your DSC

- Create .zip file

- create upload file

- Upload file in Income Tax Portal

1. Creating Signature file for Registering DSC

First you have to create a signature file then you have to upload it in income tax portal. For creating signature file you need a software that is called DSC Utility you can download from Income tax portal or my given link. After downloading DSC Utility follow below steps.

Note: Java must be installed in your system

- First put the DSC token in you computer and then open DSC Utility

- Now click on Register/Reset password using DSC

- Now enter User ID, PAN and DSC details then click Generate Signature file

- Now submit with token password and save the signature file.

- Go to https://www.incometaxindiaefiling.gov.in/ and click on Login Here.

- Enter User ID (TAN), Password, and Captcha. Click Login.

- After Login, click on Profile Settings -> Register Digital Signature Certificate

- Now choose the Signature file and click submit.

- Now Digital signature certificate successfully updated in Income Tax portal

2. Create zip file

- Right click on the .fvu file.

- Then click on Add to archive...

- Now Select ZIP from Archive Format, then click OK

- Now ZIP file created

3. Create Signature file for upload

- Now again open DSC Utility

- click on Bulk upload

- Here select the ZIP file you have created in previous step, Provide user id and PAN number and select token and click Generate Signature file.

- Now signature file created.

4. Uploading File in Income Tax Portal

- Go to https://www.incometaxindiaefiling.gov.in/ and click on Login Here.

- Enter User ID (TAN), Password, and Captcha. Click Login.

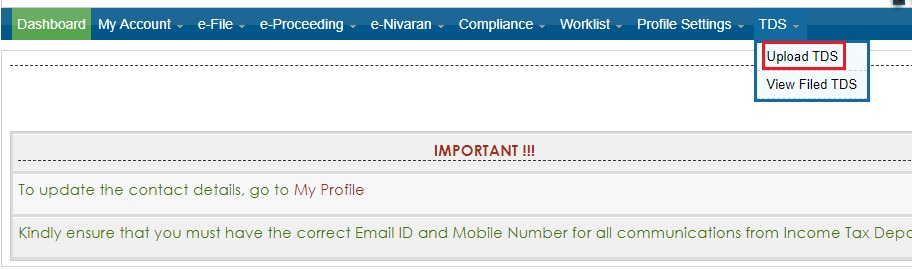

- Go to TDS > Upload TDS.

- In the form provided, select the appropriate statement details from the drop down boxes, then click on validate

- Now upload the ZIP file and signature file that you have created in step 2 and step 3

- After upload you can see like this

- To download the Provisional Receipt,

- Go to TDS > View filed TDS.

- Select the appropriate option

- Click on Token number

- Now click on Click here to download Provisional Receipt.

Note: To open the PDF, enter you TAN number in lower case.

Registration/Preparation and Filing of Income Tax SFT Report (Form 61A)

Today I am going to tell you how to file Nil return of a Sub-Registered office for the financial year 2018-19.

1. Download the Software

- Go to Income Tax Reporting Portal

- Now Click on Utilities under Resources TAB

- Here download the below 2 softwares

- Generic Submission Utility

- Report Generation and Validation Utility - Form 61A

Note: You must installed Java

2. Preparation of SFT

- Now open Report Generation and Validation Utility - Form 61A

- Here choose SFT-012 (Purchase or Sale of Immovable Property) and click Continue

- Now fill all the details in Statement (Part A) Tab

- Reporting Entity Name: Office Name

- ITDREIN: Income Tax Department Reporting Entity Identification Number is a 16 character identification number allotted by the Income Tax Department to a Reporting Entity for reporting on reportable transaction of a specified type. You have generate it from Income Tax site.

- Registration Number: blank

- Statement Type: N - Not applicable as this is a new statement/test data/there is no data to report

- Statement Number: 2019/01 (first year then numeric value 1, 2, 3...

- Reporting period ending on: FY end date means 31 March 2019

- Now put the details of Principal officer means DDO of this office

- Now click on Save button

- then click Generate XML

3. Generating ITDREIN

4. How to Digitally Sign XML file

- put your DSC Token

- open Generic Submission Utility

- here browse the XML file and click on Generate Package

- Now save the package

5. Register DSC in Reporting Portal

- Put your DSC token in computer

- Open Internet Explorer

- Now Click on Tools - Internet Options - Content - Certificates

- Now Click on your DSC Token Name and click Export

- Now Certificate Export wizard dialog opens

- Then Click Next - Next - Next - give file name and browse for save

- Now login in with Principal Officer PAN to the Income Tax Reporting Portal

- Now click on Profile - Upload Digital Signature - upload

6. Uploading Package in Reporting Portal

What is SFT report (Form-61A)

The Income Tax Act has framed a new concept to furnish a Statement of Financial Transactions in a prescribed form 61A also known as AIR (Annual Information Return) previously. The Statement of Financial Transactions or Form 61A is a record of specified financial transactions that should be furnished under the Income Tax Act.

The specified financial transactions referred above are of following kinds:

- Sale, purchase or exchange of goods, right, property, or interest in any property.

- Works contract.

- Delivering services.

- Any investment or expenditure.

- Accepting any deposit or taking any loan.

Due Date to File Form 61A

This statement for the previous FY needs to be furnished within May 31st every year. In case an assessee is not able to do so, the authorities would issue a notice to such an assessee, demanding the assessee to submit the form within 30 days from issuance of such notice.

In case such assessee continues to be the assessee in default by not answering to such notice, a penalty would be levied on the assessee that would amount to INR 500/day of such default. This penalty would be calculated from the expiry of the period as stipulated in such notice.

Transactions to be reported in Form 61A

Individuals responsible for

furnishing Form 61A

|

Type

of Transaction and limit

|

Banking Companies and Co-operative

Banks

|

Cash payment for purchase of POs

(Purchase orders) / DDs (Demand drafts) for amount totalling to INR 10 lakhs

or more annually

|

Banking Companies and Co-operative

Banks

|

Cash payment exceeding INR 10 lakhs

for purchasing any prepaid RBI instruments like RBI bonds, etc.

|

Banking Companies and Co-operative

Banks

|

Deposits or withdrawals amounting to

INR 50 lakhs or more from a current account of an account holder

|

Banking Companies, Co-operative Banks

and Post Offices

|

Deposit totalling to INR 10 lakhs or

more in one or more accounts of an account holder

|

Banking Company, Co-operative Bank,

Post Master General of Post office, Nidhi

|

Cash payment aggregating to INR 1

lakh or more in a year or INR 10 lakhs or more against any credit card bill

which is issued to a customer in a year

|

A company or an institution issuing

debentures or bonds

|

Receipt exceeding INR 10 lakhs in a

year from an individual for acquiring such debentures/bonds

|

A company issuing shares

|

Receipt exceeding INR 10 lakhs in a

year from an individual for acquiring such shares. This includes share

application money received.

|

Listed companies

|

Share buy-back from a person for an

amount totalling INR 10 lakhs or more

|

Manager/Trustee of a Mutual Fund

|

Receipt exceeding INR 10 lakhs in a

year from an individual acquiring the units of such Mutual Fund

|

A Dealer of Foreign Exchange

|

Receipt from a person for sale of a

foreign currency or expenses incurred in such foreign currency via a

debit/credit card or via issue of draft or traveller’s cheque or any other

financial instrument for an amount totalling INR 10 lacs or more annually

|

Inspector-General/Sub-Registrar

appointed under the Registration Act, 1908

|

Sale/ Purchase by a person of an

immovable property for INR 30 lakhs or more or which is valued by stamp

valuation authority at INR 30 lakhs or more

|

Persons liable for audit u/s 44AB of

the Income Tax Act

|

Cash receipt exceeding INR 2 lakhs by

a person for sale of goods or rendering of services (other the ones specified

above)

|

Home Loan Tax Calculations

1. Deduction of Interest Paid on Housing Loan

- A home loan must be taken for the purchase/construction of a house and the construction of the house must be completed within 5 years.

- It has two components – Interest payment and Principal repayment.

- The interest portion of the EMI paid for the year can be claimed as a deduction from your total income up to a maximum of Rs 2 lakh under Section 24

- Additional exemption of upto Rs. 50,000 under Section 80EE

- Value of this house should be Rs 50 lakhs or less

- Loan taken for this house must be Rs 35 lakhs or less

- The loan must be sanctioned between 01.04.2016 to 31.03.2017*

- As on the date of the sanction of loan, no other house property must be owned by you.

- The Principal portion of the EMI paid for the year is allowed as deduction under Section 80C.

- The maximum amount that can be claimed is up to Rs 1.5 lakh

The house property should not be sold within 5 years of possession. Otherwise, the deduction claimed earlier will be added back to your income in the year of sale.

Example:

If Ram taken a house loan. Total Loan Value: 5 Lakh, Year: 10 Year

During FY 2018-19, he pay total 80,000/- as loan amount from that Interest Amount: 30,000/- and Principal Amount: 50,000/-.

Adjustment:

In 24B: 30,000/- (limit upto 2 lakh)

80C: 50,000/- (limit upto 1.5 lakh)

Some tables for easy understanding

Type of Property

|

Self Occupied Property

|

Not Self Occupied Property

|

||

Completion

Status

|

Completed

within 5 years

|

Not

completed within 5 years

|

Completed

within 5 years

|

Not

completed within 5 years

|

Deduction

Allowed

|

Rs.

2,00,000

|

Rs. 30,000

|

No Limit

|

No Limit

|

Particulars

|

Section

24

|

Section

80C

|

Tax

Deduction allowed for

|

Interest

|

Principal

|

Type of

Property

|

Any Real

Estate Property

|

Only

Residential House Property

|

Basis of

Tax Deduction

|

Accrual

basis

|

Paid basis

|

Quantum of

Tax Deduction allowed

|

Self

Occupied Property:Rs. 2,00,000. Non Self Occupied Property: No Limit

|

Rs.

1,50,000

|

Purpose of

Loan

|

Purchase/

Construction/ Repair/ Renewal/ Reconstruction of a Residential House

Property.

|

Purchase /

Construction of a new House Property

|

Eligibility

for claiming Tax deduction

|

Purchase/

Construction should be completed within 5 years

|

Nil

|

Restriction

on Sale of Property

|

Nil

|

Tax

Deduction claimed would be reversed if Property sold within 5 years

|

Particulars

|

Quantum of Deduction (Rs.)

|

|

Self Occupied Property

|

Non-Self Occupied Property

|

|

Section 24

|

2,00,000

|

No Limit

|

Section 80C

|

1,50,000

|

1,50,000

|

Section 80EE

|

50,000

|

50,000

|